- The fresh mark several months: You need to use the fresh new account so you can borrow and pay-off money freely. This period normally lasts 10 years, from which area the loan motions towards cost period.

- New payment period: You could no further borrow secured on the credit line during this date, and ought to pay off brand new the equilibrium. New repayment months generally speaking persists twenty years.

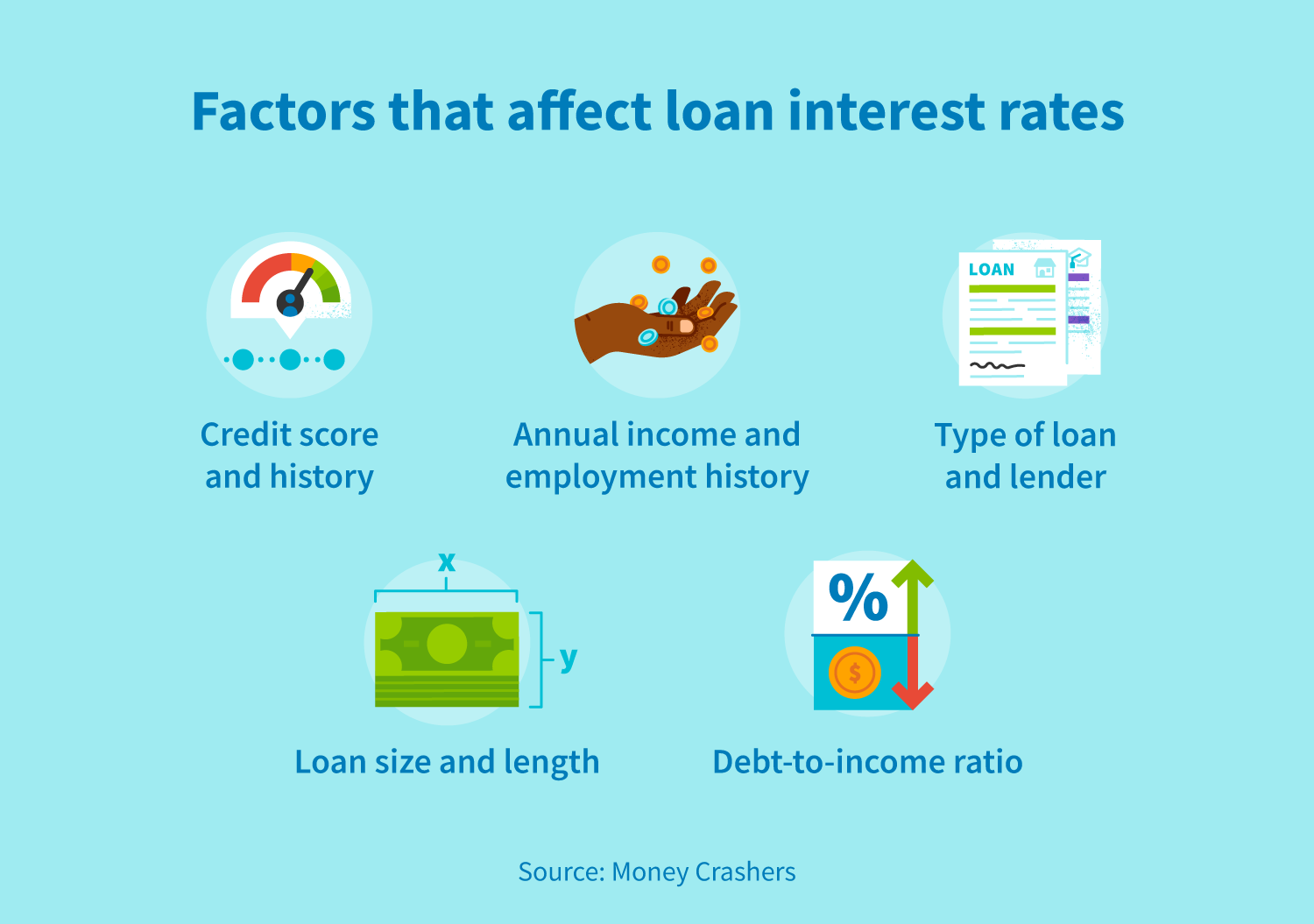

The interest rate you might be given depends on the fico scores, earnings, and the lender’s formula

Rates on HELOCs usually are variable, associated with published market costs and you can already start from a decreased of 2.5% up to 21%.

An element of the difference in property security line of credit and you can an effective HELOC issues the way you receive and repay everything you borrow. With respect to the way you should use the lent fund, one or the almost every other can be a bit more reasonable with regards to of interest charges.

Which have a property security mortgage, you can get a complete level of your loan since the mortgage is approved, and you have to repay it more an appartment number of fixed monthly payments. Fees episodes generally may include four in order to a decade, but 20- as well as 31-year terms try it is possible to. The level of interest you can easily shell out along the life of new loan is essentially known from the beginning; you’re able to save yourself particular attention from the settling the latest loan early, however some lenders charge punishment having using funds regarding before agenda.

Which have an effective HELOC, you could potentially potentially save money on notice charge for individuals who maintain your withdrawals relatively small and lower your own stability between expenditures.

You’re able to subtract attract repayments to your household guarantee personal lines of credit and HELOCs after you document the federal income fees, exactly as you do pri, it is possible to simply subtract interest to your home equity loans otherwise HELOCs in the event the loan proceeds are accustomed to build home improvements. Your own overall annual deduction to the desire regarding all home loan, home security and HELOC funds cannot meet or exceed $750,100.

Choice Particular Loans

Family collateral finance and HELOCs is going to be welcome resources of ready cash to possess being qualified home owners, nonetheless carry significant risks: If you are struggling to match your instalments with the a house equity loan otherwise HELOC, the lending company gets the directly to foreclose and take possession of your home.

- Personal bank loan: A personal loan is actually a form of unsecured borrowing from the bank, and therefore it doesn’t need you to establish property as the collateral resistant to the debt. Mortgage amounts ranges of $1,000 in order to $ten,100, and rates of interest are different generally, centered on credit score and you can money top. You may be in a position to be considered with a good credit rating, but a credit rating from the a great variety otherwise greatest commonly leave you accessibility a greater range of possibilities.

- Line of credit: Banks and borrowing unions enable it to be individuals which have good credit to open up personal lines of credit-rotating borrowing from the bank account which do not want collateral or that use the new belongings in a certification out-of deposit (CD) because guarantee. Such as for instance HELOCs, these personal lines of credit allow distributions and payday loans Mount Crested Butte costs in the varying quantity, and just fees interest towards the stability. Lines of credit possess limited draw and you will cost episodes, being typically less than others getting HELOCs-only three to five ages each.

- Peer-to-peer funds: These could become got through online creditors that meets traders looking to point finance which have individuals seeking to fund. Known as peer-to-peer otherwise P2P lenders, those web sites do not check always credit scores, nonetheless create generally speaking need proof of money or any other possessions. Peer-to-peer networks will be a beneficial capital to own less funds (normally $5,100000 otherwise shorter). Cost symptoms on P2P money are usually fairly brief, 5 years otherwise quicker.